In the United States, an adhering mortgage is one which fulfills the recognized rules and treatments of the 2 significant government-sponsored entities in the real estate financing market (including some legal requirements). In contrast, lenders who choose to make nonconforming loans are working out a greater threat tolerance and do so understanding that they Click here for info face more difficulty in reselling the loan.

Managed lending institutions (such as banks) may go through limitations or higher-risk weightings for non-standard home mortgages. For example, banks and home loan brokerages in Canada deal with restrictions on providing more than 80% of the residential or commercial property value; beyond this level, home mortgage insurance is generally required. In some countries with currencies that tend to depreciate, foreign currency home mortgages prevail, allowing lenders to lend in a stable foreign currency, whilst the customer handles the currency threat that the currency will depreciate and they will for that reason need to convert higher amounts of the domestic currency to repay the loan.

Total Payment = Loan Principal + Expenditures (Taxes & charges) + Overall interests. Fixed Interest Rates & Loan Term In addition to the two standard methods of setting the cost of a home mortgage loan (repaired at a set rates of interest for the term, or variable relative to market rates of interest), there are variations in how that expense is paid, and how the loan itself is paid back.

There are also numerous mortgage payment structures to fit various kinds of customer. The most typical method to pay back a safe mortgage is to make regular payments towards the principal and interest over a set term. [] This is commonly described as (self) in the U.S. and as a in the UK.

Particular details might specify to various places: interest might be computed on the basis of a 360-day year, for example; interest may be intensified daily, yearly, or semi-annually; prepayment penalties might apply; and other factors. There may be legal restrictions on certain matters, and customer security laws may define or forbid particular http://www.wesleytimesharegroup.com/the-successful-leader/ practices.

In the UK and U.S., 25 to 30 years is the normal optimum term (although shorter durations, such as 15-year mortgage, prevail). Mortgage payments, which are usually made monthly, contain a repayment of the principal and an interest aspect - what beyoncé and these billionaires have in common: massive mortgages. The quantity going toward the principal in each payment varies throughout the regard to the home mortgage.

Which Banks Offer 30 Year Mortgages Can Be Fun For Anyone

Towards completion of the home mortgage, payments are mainly for principal. In this way, the payment quantity determined at start is computed to ensure the loan is paid back at a defined date in the future. This offers customers assurance that by keeping payment the loan will be cleared at a defined date if the interest rate does not alter.

Similarly, a home loan can be ended before its scheduled end by paying some or all of the remainder prematurely, called curtailment. An amortization schedule is normally exercised taking the principal left at the end of monthly, multiplying by the regular monthly rate and after that deducting the regular monthly payment. This is normally created by an amortization calculator using the following formula: A = P r (1 + r) n (1 + r) n 1 \ displaystyle A =P \ cdot \ frac r( 1+ r) n (1+ r) n -1 where: A \ displaystyle is the regular amortization payment P \ displaystyle P is the principal amount obtained r \ displaystyle r is the rate of interest expressed as a fraction; for a regular monthly payment, take the (Annual Rate)/ 12 n \ displaystyle n is the variety of payments; for monthly payments over 30 years, 12 months x 30 years = 360 payments.

This type of home mortgage is common in the UK, specifically when related to a regular investment strategy. With this arrangement routine contributions are made to a different financial investment strategy created to develop a lump amount to pay back the home loan at maturity. This kind of arrangement is called an investment-backed home loan or is typically associated to the type of plan used: endowment home mortgage if an endowment policy is used, likewise a individual equity strategy (PEP) mortgage, Individual Savings Account (ISA) home loan or pension mortgage.

Investment-backed home mortgages are viewed as higher danger as they depend on the investment making adequate go back to clear the financial obligation. Up until recently [] it was not uncommon for interest only home loans to be set up without a repayment lorry, with the debtor gaming that the home market will rise sufficiently for the loan to be paid back by trading down at retirement (or when lease on the property and inflation combine to surpass the interest rate) [].

The issue for lots of people has been the fact that no payment car had been executed, or the lorry itself (e. g. endowment/ISA policy) performed badly and for that reason insufficient funds were readily available to repay balance at the end of the term. Moving on, the FSA under the Mortgage Market Review (MMR) have specified there should be stringent requirements on the repayment car being utilized.

A revival in the equity release market has actually been the introduction of interest-only life time home loans. Where an interest-only home loan has a set term, an interest-only life time home mortgage will continue for the rest of the mortgagors life. These schemes have actually proved of interest to people who do like the roll-up result (intensifying) of interest on conventional equity release plans.

How To Rate Shop For Mortgages Can Be Fun For Anyone

These individuals can now effectively remortgage onto an interest-only life time home loan to preserve connection. Interest-only life time home loan plans are presently used by 2 lenders Stonehaven and more2life. They work by having the alternatives of paying the interest on a month-to-month basis. By paying off the interest implies the balance will remain level for the rest of their life.

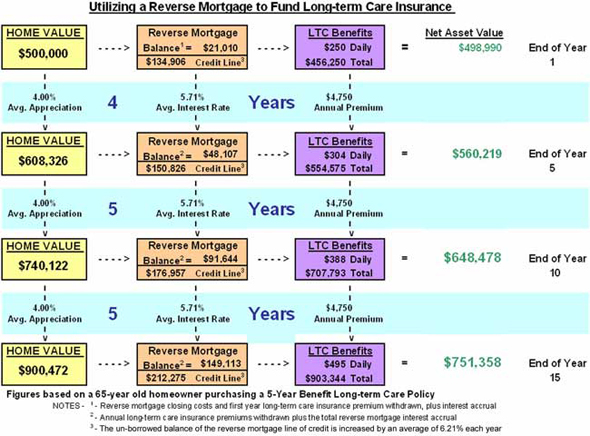

For older borrowers (generally in retirement), it might be possible to arrange a mortgage where neither the principal nor interest is repaid. The interest is rolled up with the principal, increasing the debt each year. These plans are otherwise called reverse home loans, life time mortgages or equity release home mortgages (describing house equity), depending on the country.

Through the Federal Housing Administration, the U.S. government insures reverse home loans by means of a program called the HECM (House Equity Conversion Home Mortgage) (what is the interest rate today on mortgages). Unlike standard home loans (where the whole loan quantity is normally paid out at the time of loan closing) the HECM program enables the house owner to receive funds in a variety of methods: as a one time lump sum payment; as a regular monthly tenure payment which continues until the borrower passes away or moves out of your house completely; as a month-to-month payment over a defined duration of time; or as a line of credit.

In the U.S. a partial amortization or balloon loan is one where the amount of monthly payments due are determined (amortized) over a particular term, but the exceptional balance on the principal is due eventually brief of that term. In the UK, a partial payment home mortgage is rather typical, particularly where the original home mortgage was investment-backed.